Ten minutes engaging with your super could make you $500,000 better-off in retirement.

1

How long did you shop around for your last car? How much time did you spend comparing plane tickets? How long have you spent reading reviews for pillows, or dog food, or tents?

Most people underestimate the importance of spending just a little bit of time making just one or two decisions about their super. But making the right choices can have a big impact on your quality of life in retirement.

Choosing low fees, index fund options and combining multiple accounts will have the biggest effect.

Super Basic

Superannuation. As a form of forced saving in a lower-tax account, it’s the best way to invest for retirement right now. Your employer must pay 10% 2 of your salary to your super account. You pay only 15% tax on this money, instead of your marginal income tax rate. In 2021-22, these marginal rates start at 19% once you earn over $18,200 per year, rising to 45% over $180,001 – not including the 2% Medicare levy. Making extra contributions to your super account is generally considered tax effective if you earn over $45,000 per year (recently increased from $37,000 due to tax bracket changes).

The ‘catch’ is that you cannot access your super until you retire. But that means more time for compound interest to work its magic.

Australia’s superannuation system is generally considered one of the best retirement schemes in the world. 3

But it’s not perfect. For one, Australians pay too much in super fees: about $2,400 each, every year, with an average fee of about 1%. For the whole country, that’s over $30 billion. 4

These fees reduce the returns of your investment and leave you with less money in retirement. That’s because even small differences in fees can have a big impact over decades.

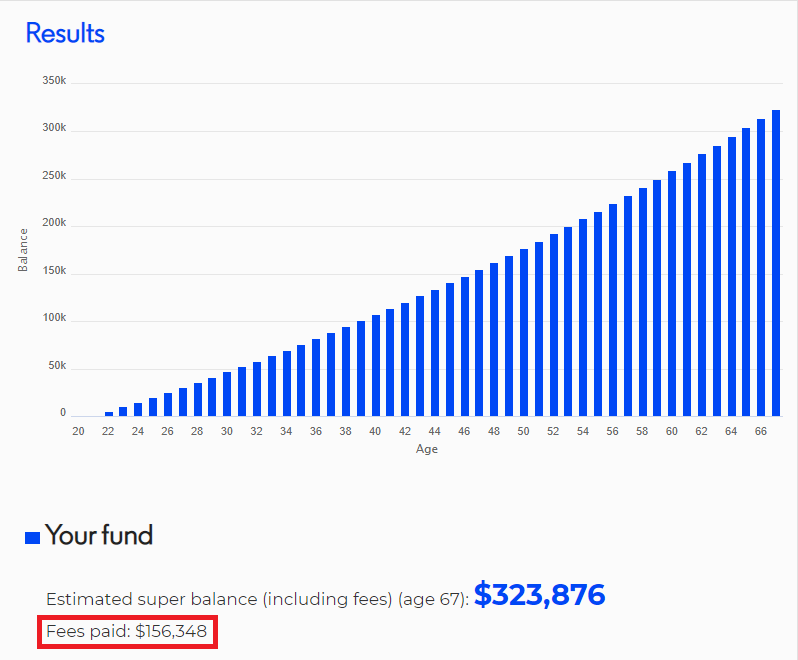

Let’s say you’re 21 and starting your first job earning $50,000. You keep that income for the rest of your working life, until you retire at 67. You get 10% of your salary in super (in reality, this would eventually go up to 12%) and your fund is returning 7%. Have a look at the difference between 0.07% and 1.5% fees. Funds offering both of those options exist today.

The difference in fees paid? $125,397.

That’s what you could save – not bad for a few minutes’ work. And that number will be even larger if you ever make more than $50,000 or make any voluntary contributions.

So, how do you get these lower fees?

You switch to an indexed option in your super fund. You tell the super fund how you want your money invested, and they move your money. It’s as simple as that.

Each investment option has a different cost: options that need people to make decisions and fiddle with investments are known as active management and are generally much more expensive than passive management, which automatically tracks the entire index of a stock market. These passively managed funds are usually called index funds.

But because they’re managed by people, almost all the default MySuper fund options are actively managed. That means higher fees, and, as we’ll get to in a second, worse results.

But first, get this: two-thirds of Australians have never switched their super fund option. 5 That means lots of people end up in underperforming funds, with high fees or bad investment returns. In the worst case, this can make someone over half a million dollars poorer in retirement. Join the one-third taking control of their future.

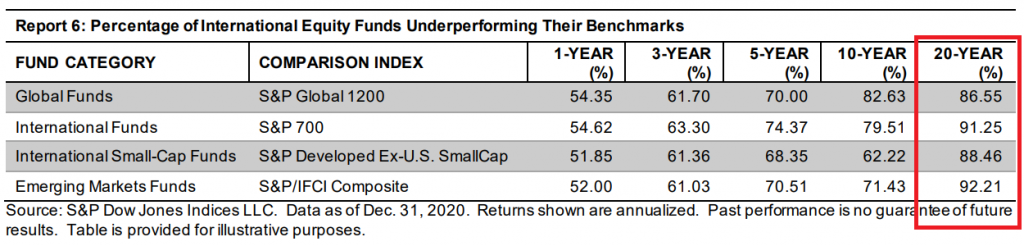

Back to those results. Over the long-term, how do active and passive management compare? How will MySuper options compare to an index option?

Have a look at the data. This is the percentage of American actively-managed funds that underperform the market’s index.

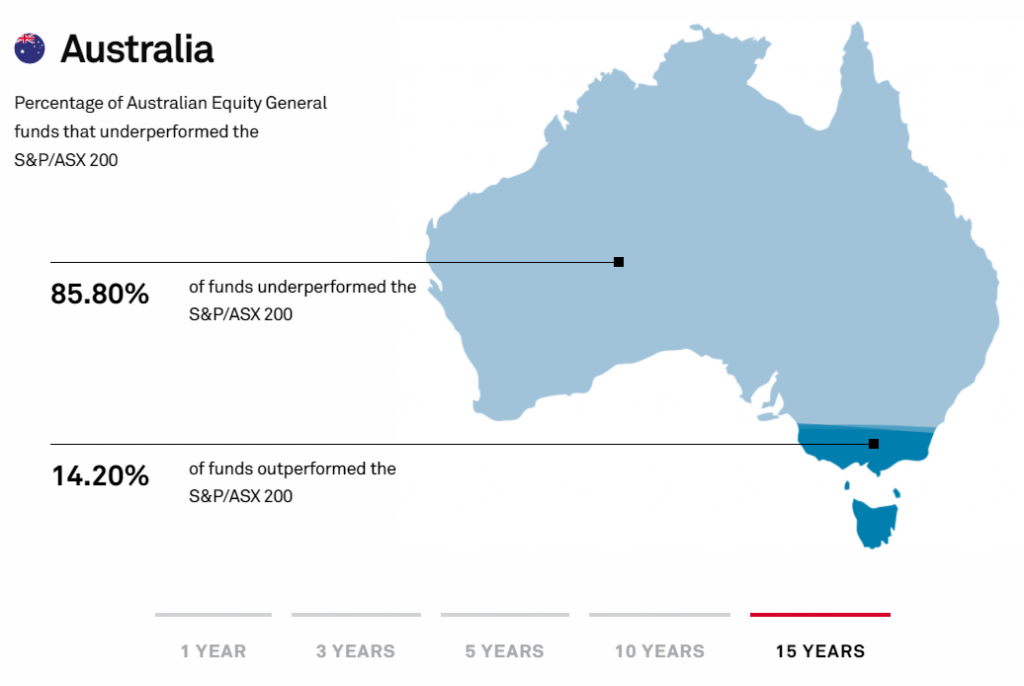

How about Australia?

The SPIVA Scorecard compares actively managed and index funds around the world. In Australia, over a 15-year timeframe, less than 15% of actively managed funds outperformed the index. And the longer your timeframe, the fewer the outperformers.

So, whether you’re investing in the US or Australia, passive management almost always provides better returns over the long run. That’s why you should switch to your super fund’s index option.

If your super fund has no international index option, consider switching funds.

Switching super

Choosing a super fund is hard. Harder than it should be. Most of the comparison sites are businesses selling you something, and there’s nowhere impartial to easily compare the best fund options. 6 The government has, at least, made it easy to switch super funds. Most large funds will automatically transfer your other accounts into your new one when you sign up. Thankfully, which super fund you choose matters much less than the investment option you choose within it.

When comparing super funds, you should compare costs for the international index option. It generally has the lowest cost, and, over the long term, investing in a wide range of markets is much safer than concentrating your investment in just one. 7 Australia makes up less than 2% of the world’s economy, and about 44% of our economy is banks and mining. Australia has performed very well – over the last 121 years since 1900, we’re in the top few countries. But many of those exceptionally strong years were before 1971, and nobody can tell the future. 8 So, it makes the most sense to pick the international index option in your super. 9

Here are the eight funds out of Australia’s largest 20 with the lowest fees for international index options. Some of the funds had no international index option.

| Fund name | AustralianSuper | Aware Super | Australian Retirement Trust (QSuper + Sunsuper) | Unisuper | Hostplus | Rest | Spaceship | Future Super |

|---|---|---|---|---|---|---|---|---|

| Int’l index option cost | 0.44% | 0.07% | 0.11% | 0.57% | 0.07% | 0% | 0% | 0.2% |

| Total cost (+ admin. & other fees) | 0.48% | 0.22% | 0.21% | 0.57% | 0.07% | 0.12% | 0.577% | 0.885% |

| Admin. % fee cap p.a. | $8,000 | $750 | $8,000 | N/A | N/A | $300 | N/A | N/A |

This all seems too easy. What’s the catch? The only ‘catch’ is that an international index fund option will be more volatile than a MySuper option. While this means greater gains when times are good, it will also dip more than MySuper products during recessions. So it’s important to know your own risk tolerance. If you think a months-to-years-long drop of 30 or 50 percent would make it hard for you to sleep at night, consider staying in a MySuper option – or, better yet, switching to a ‘balanced’ indexed option, which will keep your fees lower than MySuper but mix in defensive assets like bonds, meaning you’ll have lower volatility overall. The worst thing you can do when the market is down is panic and change your super option, or otherwise take money out of the market, making your paper losses real. It’s your retirement money, after all – you need to take a long-term view.

Part of the magic of super – and how the system is designed to work – is that it’s harder for consumers to fiddle with their money, or take it out entirely. As shown above, over the long term you cannot time the market, so it’s best to continue steady contributions and stay the course in your chosen option, no matter the market conditions.

Consolidate your accounts

Forty percent of all super accounts are duplicate11: that means one person is paying for two or more accounts and paying two or more sets of fees. As we’ve covered, paying too much in fees can have a large impact on your final super balance. But why even bother finding a few thousand in super that’s just getting eaten up by fees anyway? Well, a small amount added early to your super can have a huge impact. This chart shows the value of one dollar at retirement by the age you invest it.

| Age | Value of $1 |

|---|---|

| 18 | $26.59 |

| 25 | $16.31 |

| 35 | $8.12 |

| 45 | $4.04 |

| 55 | $2.01 |

| 65 | $1 |

That’s a huge return for investing early. See this chart for a good visual representation. Of course, thanks to inflation, assuming historical average long-term inflation of 2.5%, $1 in 40 years will be worth just 37 cents. But it’s a powerful example of the importance of time in the market – time for compound interest to work its magic – and of the importance of investing your money as a safeguard against inflation. 12

The super industry peak body estimated the average lost super amount found in 2020 was $1,600 – but some had over $100,000. Let’s say you find the average, just $1,600, in lost super at 25. Rather than being eaten away by fees and junk insurance, that $1,600 becomes $26,000 by 65.

But who hasn’t worked a string of summer jobs? Who can keep track of all those accounts? Thankfully, like changing super funds, finding lost super accounts is very easy. Many super funds offer an option to let members automatically search for lost super. You can also use MyGov, a phone hotline or a paper form. There’s over $13 billion in lost super – find out if any of it is yours. 13

In Summary

These are the simplest things you can do to have a more comfortable retirement. In terms of dollars-per-hour, they might be the highest-value things you can possibly do.

Index fund option

Index funds beat active management in the long-term and have very low costs. Choosing them in your super is the best way to come out ahead.

Focus on low fees

Over the long-term, super-low fees will have a huge impact on your final super balance. Aim for below 0.3%.

Consolidate accounts

Even if it’s only a few thousand dollars, lost super added early enough can add up. And it’s never been easier to look for it.

F.A.Q

What to keep in mind when investing in index funds

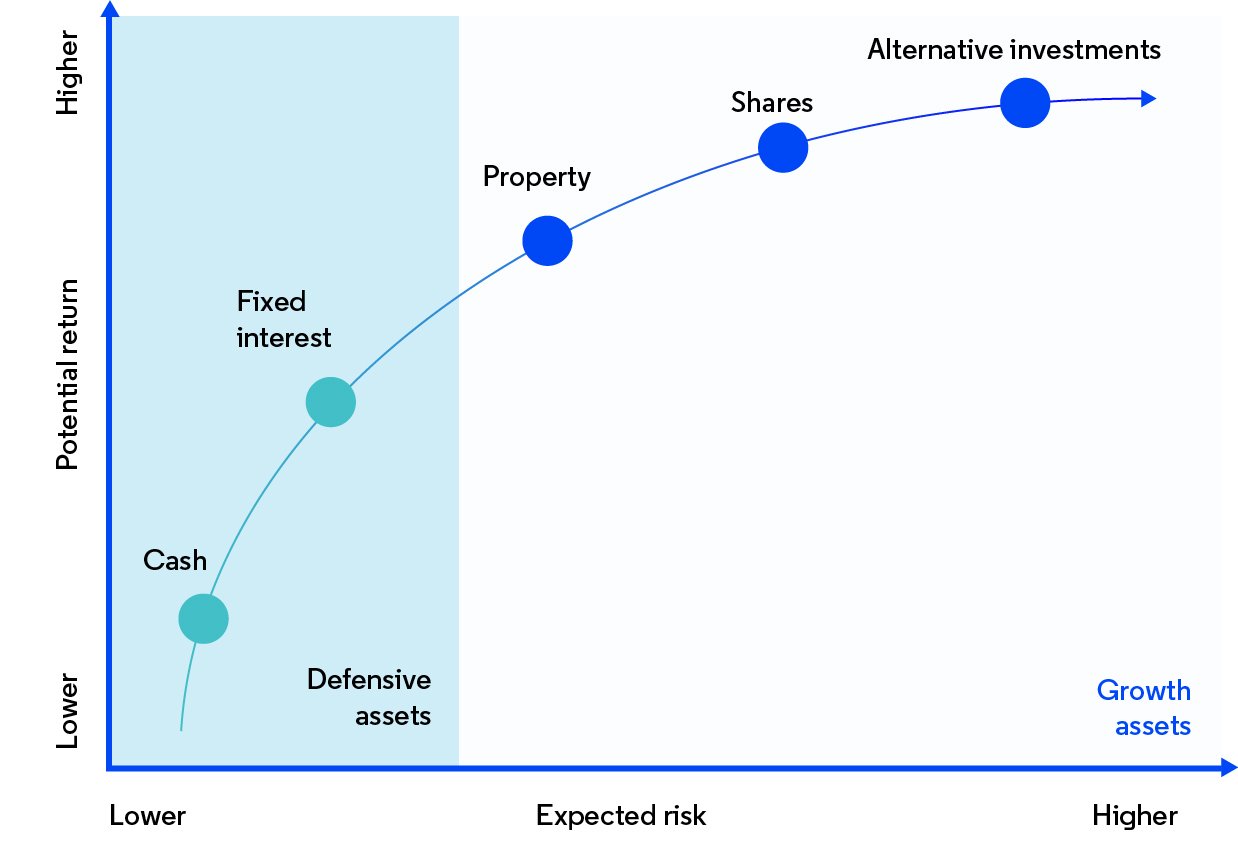

Like any investment in the stock market, index funds can go up or down. On the risk-return curve, shares are near the top of the risk-return curve (‘alternative investments’ are things like cryptocurrency and speculative stocks).

In general, though, investing in an index fund option is ‘safer’ than individual stocks. Short of the apocalypse, you’re never going to lose all of your money investing in an index. But a stock can certainly go to zero – companies go bust all the time. On average, you will have negative returns six out of every 20 years. As you approach retirement, perhaps 10 years out, so you reduce the impact of stock market fluctuations on your super value (and avoid the worst-case scenario of having to delay retirement because of a stock market crash!), you should gradually make bonds or other safe assets a greater percentage of your portfolio. Most super funds will have a ‘transition to retirement’ program which does this automatically.

You should know that by putting your super in index funds, it will be more volatile – bigger ups and downs – than having it in a MySuper option. But this also limits growth. Over the long-term, index funds will come out ahead. You should try to get a sense of your own risk tolerance: when the market is down, the worst thing you can do is take money out of the market, which ‘realises’ your losses.

It can be tempting to check your day-to-day super balance. If that’s motivating for you, that’s fine – but be careful about letting it influence your emotions too much. If you don’t think you could stomach your super losing 20% on paper for a couple of years, consider allocating 20% of your super to a bond index fund to reduce volatility. You can also go back to higher-fee MySuper options, which are usually made up of international stocks plus a whole range of other assets such as property, domestic stocks, bonds and cash. MySuper will usually deliver lower returns with a lower volatility.

Research has shown 14 that investing regularly will leave you with more money than trying to move money around. Time in the market beats timing the market.

The first rule of compounding: Never interrupt it unnecessarily.

Charlie Munger, investing partner of Warren Buffet

Retail vs industry funds

Retail super funds are run for shareholders (not members), and industry funds are for members.

If you are in a retail fund, get out. On average, their fees are double that of industry funds. 15 They justify these fees with promises of higher returns and beating the market. Unfortunately for them and their members, active management has been proven, time and time again, to underperform the market in the long run. 16 On average, retail fund returns are 2% lower than industry funds, and of member accounts underperforming the benchmark of 2005-17 returns, 77% were in retail funds. Over a long time, this underperformance could make you over half a million dollars poorer in retirement than someone in a not-for-profit industry fund. 17 If you’re in a retail fund, you’re probably giving the people running it too much of your retirement.

Insurance in your super

I am not qualified to tell you if you need insurance through your super account, but many people find it a convenient way to get coverage for things like income protection, total and permanent disability (TPD) and life insurance. Twelve million Australians have some form of insurance through their super. 18 Some people argue that having lots of people signed up through super for insurance helps to keep premiums down for everyone, and that automatic enrolment has helped address an underinsurance gap in Australia.

But not everyone gets good value from this insurance. The insurance premiums come out of your super, reducing the balance. This has a particularly large effect on low-income fund members, or those with intermittent work, who both have their total super balance reduced by premiums while not working and often face stricter criteria to claim on that insurance (there are usually clauses that make it harder to claim if you haven’t worked for 3, 6 or 9+ months). The Productivity Commission estimates this could reduce a low-income fund member’s total super balance by $85,000, or $125,000 if they also have duplicate insurance policies.

Speaking of – 17% of MySuper fund members had duplicate insurance policies across multiple accounts, leading to a retirement balance up to $50,000 lower. Some members are defaulted into insurance they cannot claim, with income protection insurance the worst offender. This is because members can usually only claim one income protection policy and, even then, only when they’re working. From the report: “A typical full-time worker can expect insurance to erode their retirement balance by $60,000 if they have income protection cover, compared with $35,000 if they only have life and disability cover.”

Nine million Australians hold TPD (disability) insurance, 86% through super. But ASIC, the financial regulator, found that the much stricter disability tests applied by some super funds would lead to 60% of TPD claims being rejected – instead of 12% under a standard test. These most often affect people who are working part-time or casual hours, are out of the workforce, are working in ‘hazardous occupations’ or are full-time carers. So make sure you read the insurance documents and work out what fits your needs.

If you have no dependents, life insurance is probably unnecessary, but some people like to keep some low level ($20,000-$50,000) for peace of mind to avoid funeral bills.

Keep in mind that as long as you’re over 25 and with a balance of over $6,000, you automatically get insurance through your super. This means you don’t have to have any medical tests; you can walk straight in. This is generally much easier than getting insurance outside of your super.

When closing any super account, you should make sure that you don’t need any of the insurance that might come with it – people sometimes keep a separate super account just to access particularly relevant insurance. This might be a rare case, but you should speak to a financial or insurance adviser. This becomes more important as you near retirement and some insurers stop accepting older members.

Ethical super – is it worth it?

There is a long-running debate about whether ethical investing, also called ESG investing (environmental, social, governance) or sustainable investing, has real benefits or is just a marketing trick to attract well-meaning, environmentally-conscious consumers.

I will go into more detail below, but the short answer is that if ethical funds are the reason you invest, invest in ethical funds. You will probably have lower returns in the long run, but it’s much better than not investing at all. If you either don’t care or think that ESG is just a marketing trick, invest in the regular market. You can donate to a cause you think is deserving, which will potentially have more tangible benefits than changing your investment style.

People arguing in favour of ESG investing say that it’s a powerful signal to companies and the market that consumers care about the environment. There have been massive inflows to the sustainable fund industry, which stands at around USD$35 trillion in 2022 and Bloomberg Intelligence reckons could exceed USD$50 trillion by 2025.

Those against it say it distorts the market, undervaluing polluting companies. Those undervalued companies then become a nice little profit-maker for other funds – and there are always other funds. 19 For more detail, NYU finance professor Aswath Damodaran has a good ESG-skeptic take on his blog. A recent WSJ column concludes that “if ESG investing truly offers rewards to investors, it brings no virtue. If it is virtuous, expect a lower reward.”

I am a cynic, particularly when it comes to advertising. Ethical investing advertising disproportionately targets young people. This is probably because young people care more about the environment and social issues. But young people are also the highest-value clients. Like the banking and insurance industries, the super industry knows that the lifetime value, the total value of a customer, is highest when they’re young. This is because while super funds earn the majority of fees right before customers retire, super is an extremely ‘sticky’ product. That means people are very unlikely to change super funds – mostly because it’s perceived as a hassle.

‘Past performance does not guarantee future returns’ – an explainer

If you’re anything like me, your reaction to that little disclaimer is just to brush it off – they’ve got to put it there, right? Check out those returns! Yes, but it’s a bit more complicated than that.

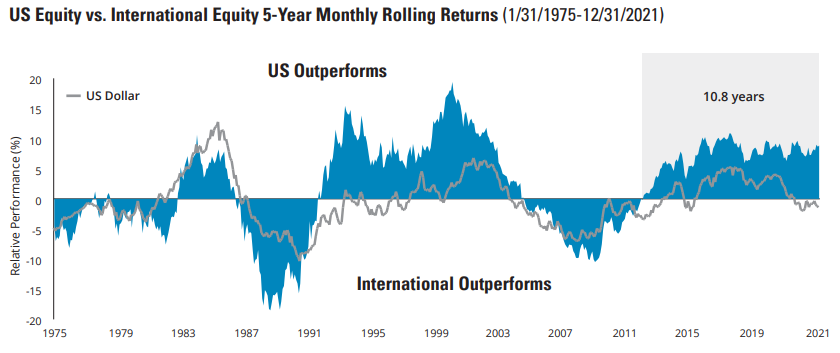

Counterintuitively, the best place to put your money is actually in assets that have recently underperformed. Jumping around, chasing the highest return number year-to-year is like trying to surf on a wave that’s already finished breaking. You’re just left with foam and sand.

This chart illustrates this principle well. You might see the US’ returns over the last few years and think ‘wow, I should jump on that train’. But, really, looking at the chart it’s clear the pendulum is overdue for a swing back in the other direction.

As Australian investors, this doesn’t really matter for us – international index funds capture both US and international (that is, equity markets outside the US) markets. The other nice thing is that, when investing for the long term – for something like retirement – even these swings in performance become negligible. Even if you make a ‘mistake’ and invest in US stocks right as they start underperforming, all it will do is let you accumulate more US stocks while they’re ‘cheaper’ – that is, undervalued. As long as you keep your money in the market, you can’t really go wrong in the long run. 20

You can get more good info on diversification and US vs non-US performance from Vanguard Research. Spoiler: “we expect that investors who maintain globally diversified equity portfolios will be rewarded in the years ahead.”

A note on inflation

Inflation is rising sharply around the developed world. Although some economists expect it to improve by 2023, many consumers are already feeling the pinch of higher prices. The best way to protect the value of your money during periods of inflation is to avoid cash and keep your assets in equities (stocks, index funds etc), commodities or real estate. But don’t overreact; putting your entire retirement into gold is likely to be a mistake (remember: pulling funds out of the market when things get shaky is a near-guaranteed way to lose money in the long run).

On super fund concentration

There’s a growing trend of super funds merging. This is a good thing for consumers, as it means super funds are facing competition to cut costs and provide more competitive returns. In general, a larger fund with more assets under management will be able to offer the same services for lower fees. Many smaller super funds are only able to keep existing because super is a very ‘sticky’ product – consumers rarely change super funds. Consider, for example, how only one third of Australians have ever switched fund options, let alone entire funds! For consumers, it’s generally safest to go with a large industry super fund, but always check the fees and the PDS. Vanguard, an American company that invented the index fund as we know it today, is set to enter the super market in 2022. They’re sure to have competitive rates, so keep an eye out.

Catch-up contributions

In 2021-22 you can contribute a maximum of $27,500 ($25,000 in the past few years) to your super at the 15% tax rate. Contributions beyond that are taxed at your income tax rate. However, as long as your super balance is under $500,000, if you didn’t use your entire cap at any point in the last five years (starting in 2018-19), you can ‘top up’ that unused cap at the 15% tax rate. If you do that with after-tax income, you can claim it at tax time for a rebate. This is particularly useful if you have some spare cash, as you save a significant amount (your marginal tax rate minus 15%) by investing it in super over any other option. The ATO tracks the amount you can catch up; you can see it at myGov. Most super funds will have information on how to make additional or catch-up contributions.

Why would I lock up my money in super until I retire? Couldn’t I just invest it myself and make more money?

This question becomes most relevant when people are deciding how to invest a larger portion of money – whether it’s best off in the market after-tax, paying off a mortgage, saving up for a house deposit or ‘locked away’ in super. 21

The main incentive to invest in super is the lower tax you pay: just 15% (up to the current concessional contribution limit of $27,500 per year). If you want to save money for retirement, super is absolutely the best place to do that. Putting your money in super also has several other advantages. Similar to getting a mortgage in the ‘rent or buy’ debate, super is a form of forced savings. You won’t be able to take it out to spend on things before you retire (you can access it early in some circumstances, but the ATO has very strict criteria).

As for you earning way more investing outside of super, not only do you pay up to 30% additional tax if you take that route, but most professional fund managers can’t even beat the market average over a 20-year timeframe, so what makes you think you can? And that’s not even counting the hours spent researching stocks and the additional stress of market volatility. You can invest in stocks through your super if you set up a self-managed super fund, though that’s generally only worth doing once your super balance gets past about $400,000. At that point, go find an accountant who specialises in SMSFs. Some super funds also allow a ‘self-managed’ option, where you pick from a list of approved – usually safer – stocks.

And for not wanting to have money ‘locked away’ until retirement: in an ideal world, you should have investments outside of super. This gives you more flexibility, especially if you’re wanting to retire early.22 But any investment in index funds most reliably provides good returns if it’s left in the market for a long time – 10-plus years, preferably longer – so trying to make a quick buck is as likely to fail as to succeed.

Also, people are generally bad at thinking long-term. Do you really believe you won’t reach retirement age? Just because it seems far away, it doesn’t mean it won’t one day arrive. What would ‘future you’ want you to do?

Picking individual stocks, particularly small ones, is a very good way to lose money. If you need to scratch that itch, perhaps set up a small amount – no more than 5% of your total investment – for excitement or wild bets. Mostly, investing should be boring and long-term.

What index does an index fund track?

This is a niche – but interesting – question. Let’s say a super fund wants to let its members invest in a low-cost international index fund. They can either manage it themselves, or, more likely, the super fund will buy a product like the MSCI World index and offer that to their members.

Why does this matter? In the scheme of things, it doesn’t – but it can lead to very minor differences between the indexed ‘products’ offered by different super funds. Of course, the biggest determinant will still be super fees – but small differences between these base products (e.g. whether the base index tracks 1,550 companies or 1,600 companies) can lead to gaps of a few fractions of a percent between different funds’ indexed options, even though they’re all offering ‘International Indexed’. For me, this is not worth worrying about.

If you are a 21-year-old starting your first job earning $50,000 per year, the difference between a bottom and top quartile MySuper fund (the default option) by the time you retire is as much as $502,000. Superannuation: Assessing Efficiency and Competitiveness p. 13↩

Retirement Income Report p. 22

In a 2019 survey, Australia came in 3rd place behind the Netherlands and Denmark. Our pension system is unique, and we were one of the first to use a ‘three pillars’ approach, with a means-tested age pension, compulsory superannuation and tax incentives to encourage voluntary super saving. Australia’s approach has been endorsed by the World Bank as international best practice. Ibid. p. 84↩

Australia’s $360b super fee bill, AFR, September 2020.

Also, there’s a reason the Google AdWords cost-per-click for ‘superannuation’ is $30. It’s because new members are very profitable – think of the lifetime of fees!↩

Superannuation: Assessing Efficiency and Competitiveness p. 25↩

The current incarnation of the YourSuper tool by the ATO is a good start, but only compares MySuper (default) options. The fees on various MySuper funds are around 0.6%-1.2%, which isn’t as high as some other options – but it’s still too high. This MoneySmart page also has good information.↩

You can read more about the benefits of diversification at Moneysmart.↩

If your fund offers the option to pick specific percentages of different options, you can of course still invest in some of the Australian index – say, 90% international, 10% Australian. But many people also don’t want to concentrate their risk in Australia, especially if they already own a house and have a job tied to the Australian economy. By staying international, you’re protecting your super from shocks to our relatively small, concentrated economy.↩

Hostplus and Rest offer the lowest fees for international index options right now. I included Spaceship and Future Super even though they’re not in the top eight cheapest funds because they’re aimed at young people, whose decisions on super will have a larger impact than people closer to retirement. It was often very annoying to find and compare the specific fees you pay at different funds. Many of them had rules like ‘0.15%, only charged up to a maximum of $750 per year’, which is difficult to reflect simply. This Reddit user made an excellent detailed comparison chart. If a fund had unhedged and hedged index options, I listed the unhedged version. Some large funds (e.g. CSC, which runs Military Super and other public service funds) had no international index option and were excluded. I also didn’t include the dollar amount administration fee, usually a maximum of $70 per year, as it’s capped at a dollar amount and won’t impact your account growth the same way a percentage fee will. Other than AMP’s MySuper at 0.51%, which doesn’t seem to be accepting new members, the cheapest MySuper product was from Unisuper, at 0.65%. You can compare other MySuper products with APRA’s heatmap.↩

Superannuation: Assessing Efficiency and Competitiveness p. 17↩

This is also why putting just a little extra into super when you’re young will have a big impact on your final super balance. You can also use leftover concessional contributions from the past five years.↩

Super nerd stuff: in late 2021, the government introduced super ‘stapling’, meaning employees have one super fund ‘stapled’ to them as they move around jobs. This should massively reduce the number of unnecessary accounts and fees – but it means the choices you do make in that one fund are even more important!↩

See the Efficient Market Hypothesis or this entire website dedicated to tracking the underperformance of managed funds↩

Superannuation: Assessing Efficiency and Competitiveness pp. 7-11↩

Superannuation: Assessing Efficiency and Competitiveness pp. 19-20↩

For example, coal power assets sold off by western companies due to pressure from their consumers will not be closed down. The hydrocarbons will still be extracted, just purchased at a cheaper rate by less morally pure companies.↩

The same goes for hedged vs unhedged currency index fund options. Hedging tries to reduce the effects of currency value fluctuations. But in the long run, it doesn’t really matter.↩

If you have high-interest debt (credit card, Afterpay/BNPL, car loan above about 5%) you should absolutely pay that down first. HECS/HELP debt can generally be left alone, as it’s paid back automatically through your salary and is indexed to CPI, i.e. basically interest-free. In 2021 the indexation rate was 0.6%, but averaged around 2% for the 10 years before that.↩

For a ‘glide path’ with early retirement, there is an optimal level to invest at, where you can live off your outside-of-super money that’s invested in the market until you can access your ‘cheaper’ (tax-efficient) in-super money. But this optimal point will be highly subject to market returns, especially as you approach your retirement date.↩